Understanding Term Life Insurance: Is It Your Safety Net?

Term life insurance serves as a crucial financial safety net for individuals looking to protect their loved ones in the event of an unforeseen tragedy. Unlike whole life insurance, which provides lifelong coverage and includes an investment component, term life insurance offers coverage for a specific period—typically ranging from 10 to 30 years. This type of policy is often considered more affordable, making it an attractive option for families who want to ensure that their dependents are financially secure without the burden of high premium payments. As such, many people see term life insurance as a practical solution to safeguard their family's future financial health.

When evaluating whether term life insurance is the right choice for you, consider your personal and financial obligations. Key factors to assess include your current debts, future financial goals, and the financial needs of your dependents. For instance, if you are a parent or caretaker, you may want to ensure that your children can cover education expenses or that your spouse can manage household costs in your absence. Ultimately, understanding the benefits of term life insurance can provide peace of mind, knowing that your loved ones will have a financial cushion in place when they need it most.

Is Term Life Insurance Worth It? Exploring the Pros and Cons

Term life insurance can be a valuable financial tool for individuals seeking to provide security for their loved ones without the high costs associated with permanent life insurance. This type of policy typically offers lower premiums, making it more accessible for families or individuals on a budget. One of the main advantages of term life insurance is that it allows policyholders to cover specific financial responsibilities, such as a mortgage or children's education, during the years when those expenses are most significant. Additionally, the policy can be easily converted to permanent insurance later on, giving flexibility as financial situations change.

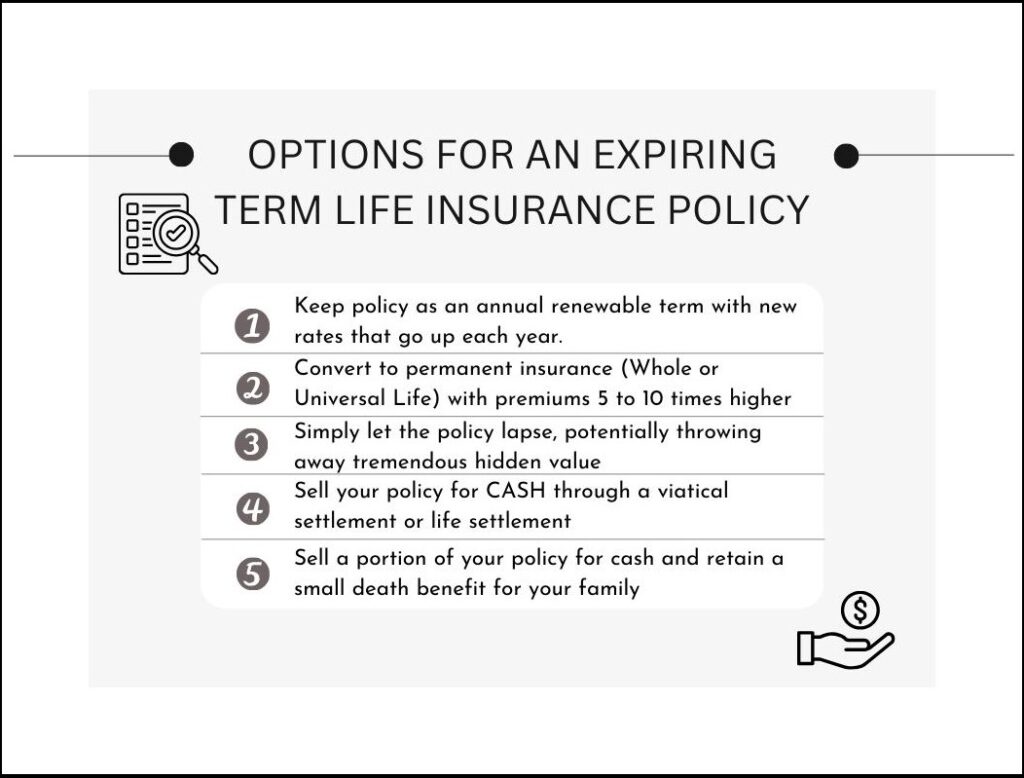

On the flip side, there are some drawbacks to consider when it comes to term life insurance. For instance, once the term expires, the coverage ceases unless renewed, and premiums may be significantly higher if you choose to extend the policy at an older age. Furthermore, term life insurance does not build any cash value, meaning there is no return on investment if the policyholder outlives the term. Weighing these pros and cons is essential when deciding if term life insurance meets your long-term financial needs and offers the necessary peace of mind for you and your beneficiaries.

What You Need to Know Before Buying Term Life Insurance

Before purchasing term life insurance, it's essential to understand what it entails and how it fits into your financial planning. Term life insurance provides coverage for a specific period, typically ranging from 10 to 30 years, making it an affordable option for those who need substantial coverage without high premiums. Prior to buying, consider the duration of coverage you need based on your financial responsibilities, such as mortgages, children's education, and other long-term financial goals. It's also crucial to assess how much coverage you require; many experts recommend a sum that is 10 to 15 times your annual income to provide adequate protection for your loved ones.

Another key factor to consider is the policy's terms and conditions. Not all term life insurance policies are created equal, so scrutinize elements such as renewal options, convertibility to permanent insurance, and any exclusions that may apply. Reading the fine print can save you from potential pitfalls later on. Moreover, it's wise to shop around and compare quotes from various insurance providers to find the best deal. This not only helps in securing a competitive rate but also allows you to gauge the insurer's financial stability and customer service reputation, which are important for long-term satisfaction with your policy.